Well, as per both previous GAAP and Ind AS recognised costs related to its post-employment defined benefit plan on an actuarial basis.

Under Previous GAAP, the entire cost, including actuarial gain and losses, was charged to the statement profit or loss.

Note: Actuarial gains or losses refer to the differences between an employer’s pension payments and the expected costs.

While, under Ind AS, remeasurements of these costs (comprising of actuarial gains and losses, the effect of assets ceiling, excluding amounts included in net interest on the net defined benefit liability and return on plan assets excluding amount included in net interest on the net defined benefit liability) are recognised in Other Comprehensive Income (OCI), which is covered under Balance Sheer under the head of shareholder’s equity.

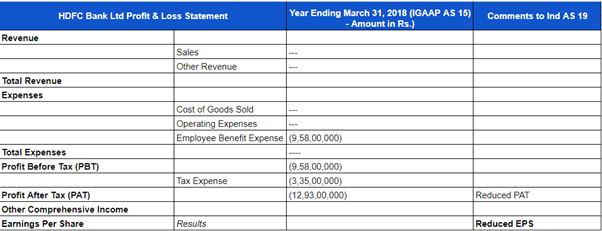

Let’s understand better with the help of an example of one of India’s leading housing finance companies, HDFC Ltd.

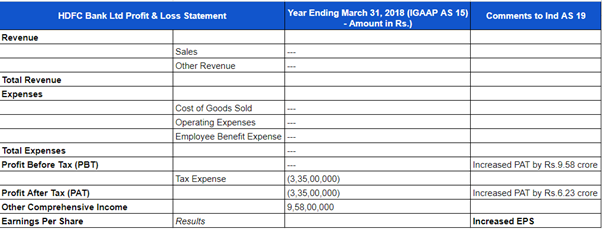

While drafting the financials for the year ending on March 31, 2018, HDFC Ltd. grouped the Employee benefit expenses of Rs. 9.58 crore as an expense under the profit and loss statement.

However, as per the adjustments under Ind AS 19, the Employee Benefit Expenses will be grouped under OCI.

Thus, employee benefit expense is adjusted by Rs. 9.58 crore and is recognised in OCI for the year ended March 31, 2018. The above change does not affect total equity as of March 31, 2018. However, profit before tax and profit after tax for the year ended March 31, 2018, increased by Rs. 9.58 crore and Rs. 6.23 crore respectively.

Financial Metric | IGAAP | Ind AS | Change |

Employee Benefit Expense | Charged fully to Profit or Loss | Adjusted by Rs. 9.58 crore and recognized in OCI | Rs. 9.58 crore less in P&L, recognized in OCI |

Profit Before Tax (PBT) | No adjustment for actuarial gains/losses | Increased by Rs. 9.58 crore due to shift of actuarial gains/losses to OCI | Increased by Rs. 9.58 crore |

Profit After Tax (PAT) | No adjustment for actuarial gains/losses | Increased by Rs. 6.23 crore (net of tax effect of adjustments moved to OCI) | Increased by Rs. 6.23 crore |

Tax Impact | Included in the statement of Profit or Loss | Regrouped to OCI, amounting to Rs. 3.35 crore | Rs. 3.35 crore moved to OCI |

Impact on Total Equity | None directly mentioned | No change in total equity as at March 31, 2018 | No change |

**Note: This example has been simplified with no additional numbers for better understanding.